Aug 8, 2025

8

mins read

In recent years, India has seen a rapid shift from cash to digital payment methods such as mobile banking, online transfers, cards, and UPI-based apps. To capture this trend, the RBI introduced a composite Digital Payments Index (DPI) in January 2021. The DPI uses March 2018 as the base year (index = 100), and combines multiple parameters to measure the extent of digitisation of payments across India A steadily rising DPI indicates wider use of online transactions and helps policymakers track progress in financial inclusion and payment infrastructure.

The Reserve Bank of India (RBI) reported that its Digital Payments Index (DPI) rose to 493.22 by March 2025, up from 465.33 in September 2024.

RBI noted that overall digital transactions grew ~11–12% year-on-year (measured by DPI) through FY2024. This reflects improved payments infrastructure and growing adoption of online transfers.

Table of content

Composite Measure: A first-of-its-kind RBI index to gauge spread of digital payments nationwide. It aggregates data on payment technology, usage, and user engagement.

Launch & Frequency: Launched January 2021, DPI is released semi-annually (with a four-month lag) on the RBI website

Base Year & Scale: March 2018 is the base period (score set at 100). Subsequent DPI values show how much digital payments have expanded since 2018.

Purpose: Tracks growth in digital payments in India – credit/debit card use, UPI transactions, mobile banking, etc. Policymakers use DPI to identify gaps in infrastructure and plan improvements.

RBI-DPI comprises five broad parameters, each with a weightage, to capture different aspects of the digital payments ecosystem:

Payment Enablers (25%) – Factors like internet and mobile penetration, and regulatory support that facilitate digital payments.

Demand-side Infrastructure (10%) – Consumer-facing infrastructure such as digital payment apps, user interfaces, and ease of access.

Supply-side Infrastructure (15%) – Merchant-side infrastructure including POS terminals, merchant apps, and payment gateway coverage.

Payment Performance (45%) – Transaction metrics: volume, value, and frequency of digital payments (e.g., number of UPI/IMPS/NEFT transfers).

Consumer Centricity (5%) – Measures how user-friendly and accessible payment systems are, including customer service and complaints mechanisms.

Each parameter consists of sub-indicators; together they offer a holistic view of digital transaction adoption

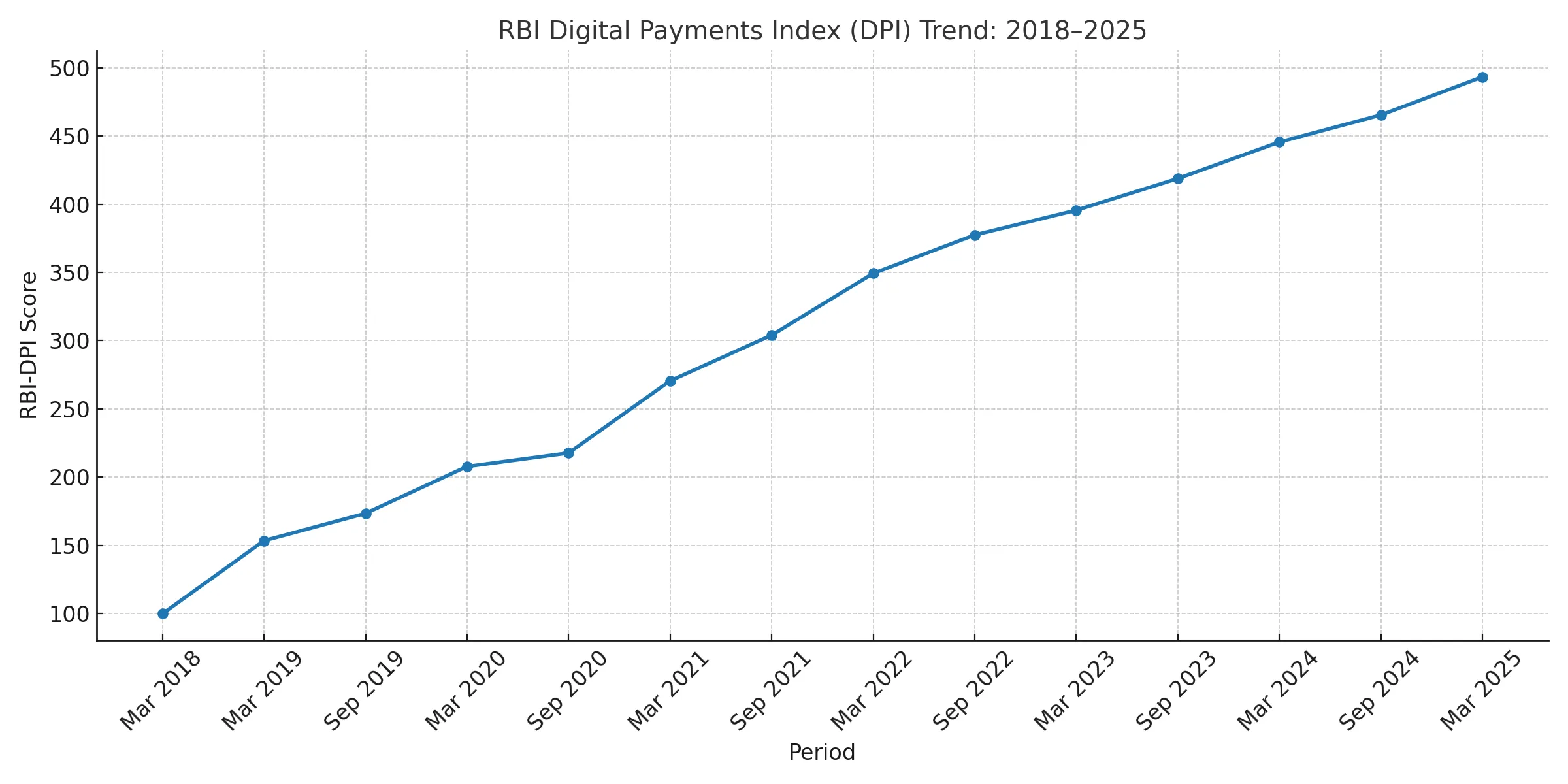

Steady Climb: Since its base of 100 in Mar 2018, the DPI has surged nearly 5×. By Mar 2025 it reached 493.22

Key Milestones: (Semi-annual data) Mar 2019: 153.47; Mar 2020: 207.84; Mar 2021: 270.59; Mar 2022: 349.30; Mar 2023: 395.57; Mar 2024: 445.50; Sep 2024: 465.33; Mar 2025: 493.22

Digital Growth: RBI reported an 11.1% increase in digital payments by Sep 2024 (YOY), attributing this to broader infrastructure and usage. Enhanced payment infrastructure and performance have driven the DPI rise.

UPI and Mobile: The explosive uptake of UPI is a key driver of DPI. UPI’s share of digital payments jumped from ~34% in 2019 to 83% in 2024, while having a 5-year CAGR of ~74%. Factors include zero transaction fees and convenient features (QR-code payments, AutoPay for recurring bills).

Unified Payments Interface (UPI): Launched in 2016 by NPCI, UPI allows instant P2P and P2M transfers via mobile apps. Users pay just with UPI IDs or QR codes. It is free of charge and supports any transaction size, boosting its appeal.

Dominant Growth: UPI has established dominance in India’s digital payments. As usage grew, it helped drive DPI higher UPI’s user-friendly design and interoperability have made it India’s leading digital payment method.

Other Methods: Payment methods like mobile wallets (Paytm, Google Pay) and card payments complement UPI. These channels have expanded merchant acceptance and online commerce, contributing to the overall digitization of transactions in India.

Accelerated Financial Inclusion: The rise in digital payments signifies deeper financial penetration and improved accessibility for underserved populations, particularly MSMEs and rural communities.

Support for Digital Credit Models: Initiatives like the New Digital Credit Assessment Model for MSMEs show a shift toward real-time, data-driven credit evaluation, supporting faster and fairer financing.

Strengthening of Digital Ecosystem: Highlights India’s evolving, resilient payment ecosystem driven by policy support, fintech innovation, and growing consumer trust.

Challenges: Despite gains, RBI notes issues like limited connectivity and awareness in rural areas, increasing frauds/data breaches, and compatibility gaps between different payment platforms. These can slow digital uptake in some regions.

Way Forward: The RBI recommends expanding internet/mobile access in villages, strengthening cybersecurity and fraud-detection, launching user awareness campaigns, and creating unified standards for seamless transactions. Implementing these can further boost the DPI.

Q: Who releases the Digital Payments Index in India?

A: The RBI publishes the Digital Payments Index semi-annually, measuring growth of digital transactions.

Q: What is the base year of the RBI-DPI?

A: The base year is March 2018 (index score set to 100).

Q: What are the major components of RBI-DPI?

A: Five parameters: Payment Enablers, Demand Infrastructure, Supply Infrastructure, Payment Performance, and Consumer Centricity.

Q: What was the RBI-DPI score in Mar 2025?

A: It reached 493.22 in March 2025

Q: How often is DPI updated?

A: DPI is updated semi-annually (every six months) with a publication lag of about four months

The RBI Index highlights India’s rapid shift towards cashless transactions. A DPI of 493.22 (Mar 2025) reflects record digital transaction volumes, driven largely by UPI and improved banking infrastructure. This composite index helps policymakers identify where to strengthen the payment ecosystem (e.g. rural connectivity, security). Continued rise in the DPI signals progress in financial inclusion and online commerce. Understanding DPI is essential for UPSC aspirants studying India’s digital economy. For more UPSC-focused insights on indices and current affairs, see Padhai Blogs.

Internal Linking Suggestions

Glacial Lake Outburst Floods(GLOFs), Meaning, Causes, Effects & Mitigation Strategies

Tsunami UPSC, Meaning, Characteristics, Causes, Impacts & Mitigation Measures

How to Begin Your UPSC Preparation : The Ultimate Guide For Beginners

UPSC Previous Year Question Papers with Answers PDF - Prelims & Mains (2014-2024)

40 Most Important Supreme Court Judgements of India : Landmark Judgements UPSC

Article 32 of the Indian Constitution: Right to Constitutional Remedies, 5 Writs, Significance

External Linking Suggestions

UPSC Official Website – Syllabus & Notification: https://upsc.gov.in/

Press Information Bureau – Government Announcements: https://pib.gov.in/

NCERT Official Website – Standard Books for UPSC: https://ncert.nic.in