Jul 27, 2025

8

mins read

What are Stablecoins?

A stablecoin is a cryptocurrency designed to hold a stable value, typically by pegging its price to a government-backed currency (most often the US dollar). The first cryptocoins appeared in 2014 (BitUSD and Tether). They function as digital assets with value backed by reserves (cash, bonds, other crypto or commodities) so they can serve as a reliable store of value within the volatile crypto market. By acting as a 1:1 bridge between “old” money and “new” crypto, stablecoins enable traders to move funds between tokens efficiently. The market has grown rapidly (over $260 billion today), prompting calls for clearer regulations.

Recent developments have thrust stablecoins into the spotlight. In July 2025, US President Trump signed the GENIUS Act requiring USD-pegged stablecoins to hold liquid reserves (e.g. US dollars and Treasury bills) and to publicly disclose them. U.S. regulators are also reported to be considering a Financial Stability Oversight Council (FSOC) review of major stablecoins (like Tether) to assess systemic risks. These moves underscore stablecoins’ growing importance as a payment tool and the need to guard against financial instability.

Table of content

Stablecoins Meaning: Cryptocurrencies aiming for price stability by pegging to another asset. They are built on blockchain networks and backed by reserve assets, usually in the same currency as their peg.

Backing Mechanism: To maintain their peg, issuers hold reserves such as cash, short-term government debt or commercial paper. For example, the recent US law mandates backing by liquid assets like USD and Treasuries.

Usefulness:

Stablecoins facilitate seamless crypto trading and transfers without volatility.

They act as a “parking place” for crypto investors to avoid traditional banking delays.

BIS notes stablecoins are “heavily used as a bridge” for trading other cryptoassets.

They are also being explored for instant payments and remittances.

Type of Stablecoin | Backing / Mechanism | Example |

Fiat-backed | 1:1 collateral in government currency (cash, bonds) | Tether (USDT), USD Coin, TrueUSD |

Crypto-backed | Crypto collateral (often over-collateralized to ensure safety) | Dai (MakerDAO) |

Asset-backed (e.g. gold) | Real-world assets like gold, commodities or bonds | Digix Gold, Tether Gold |

Algorithmic(no reserves) | Supply-adjustment algorithm, no fixed reserves | TerraUSD* (failed), Basis |

*Note: TerraUSD (UST) lost its peg and collapsed in May 2022.

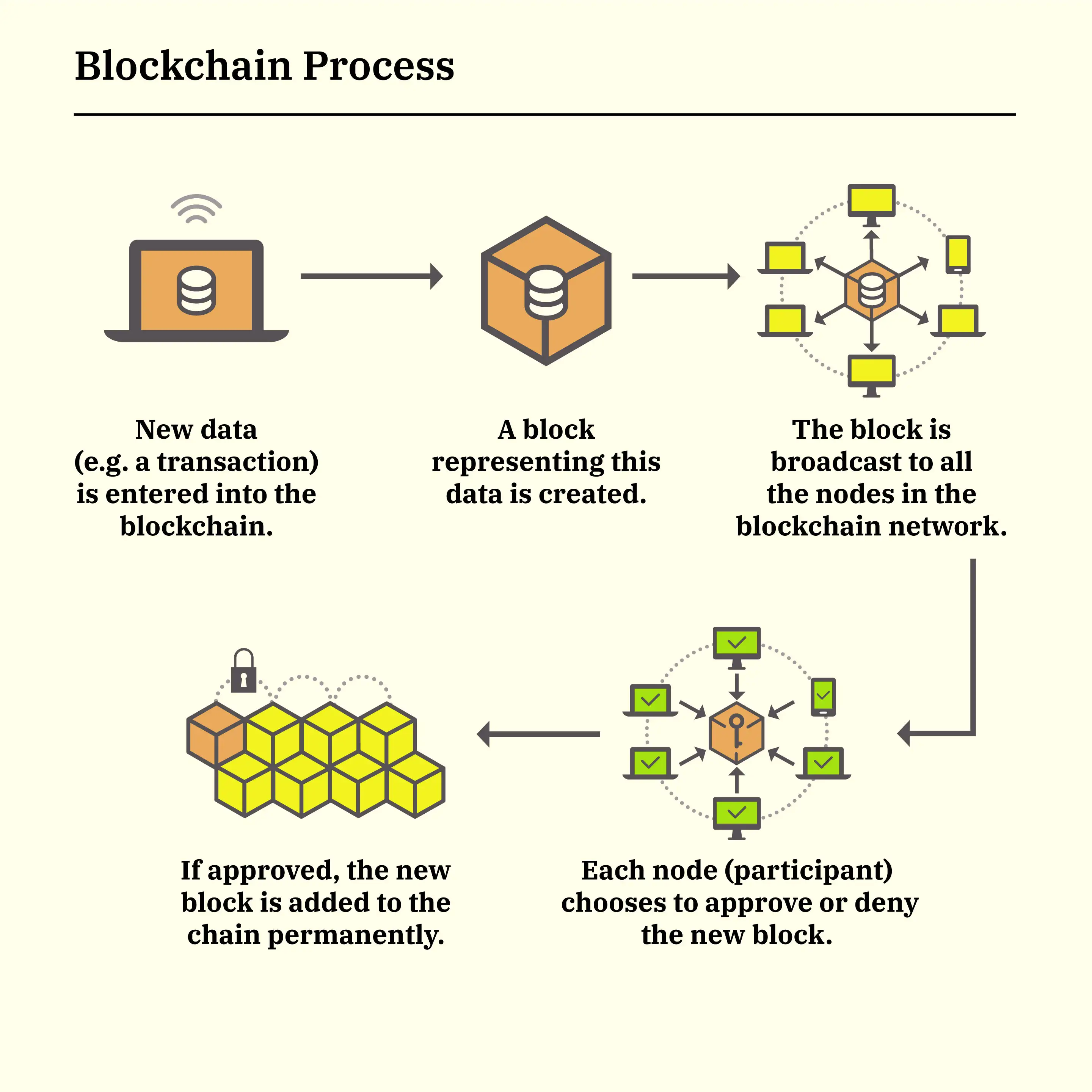

Cryptocurrencies are digital or virtual currencies that operate without a central bank, using encryption (cryptography) to regulate creation and verify transactions.

They rely on a decentralized public ledger called blockchain, which is maintained by a network of nodes rather than a single authority.

New coins are created via mining: powerful computers solve complex mathematical puzzles (proof-of-work) to validate transactions and record them on the blockchain.

Transactions are stored in a public ledger visible to the entire network, ensuring transparency and preventing double-spending.

A special type of cryptocurrency, stablecoins, aims to maintain a stable value by being pegged to assets like fiat currencies, gold, or using algorithmic mechanisms—offering less volatility and suitability as a medium of exchange.

Illiquid Reserves

Many stablecoins hold short-term debt instruments (e.g. reverse repos, commercial paper) which can dry up in a crisis.

The BIS notes most fiat-backed stablecoins hold government debt or cash equivalents.

If those markets seize up, it can trigger a run (e.g. USDC lost $5.8 billion in redemptions when Silicon Valley Bank failed in 2023).

Not Always “Stable”

No stablecoin perfectly maintains its peg at all times.

The BIS finds that “not one of them has been able to maintain parity with its peg at all times”.

Algorithmic or low-collateral stablecoins are especially prone to de-pegging.

Contagion Risk

If a large stablecoin’s reserves are liquidated in turmoil, losses could spill into other markets.

IMF analysis warns that without regulation, “contagion risks between traditional finance and the crypto ecosystem will increase.”

For example, the TerraUSD crash wiped out many crypto-collateralized coins and shrank the total stablecoin market by >20%.

Financial Stability

At scale, stablecoins could challenge monetary policy and banking.

If widely adopted, runs on stablecoins or failure of an issuer could stress banks and markets.

Regulators worry about systemic risk; the U.S. FSOC review is precisely to gauge this threat

Transparency & Accountability

Unlike banks, many stablecoin issuers provide limited audits of their reserves.

The BIS highlights a lack of standardized reporting – reserve disclosures are often infrequent or incomplete.

This opacity undermines trust: it’s unclear if issuers always have enough assets to honor redemptions.

Regulatory Challenge

Stablecoins straddle multiple domains (banking, securities, payments). There is no uniform global framework yet.

The IMF and FSB stress the need for “comprehensive, consistent, and coordinated” standards.

Different countries are moving at varying paces, making cross-border oversight difficult.

Stablecoins are increasingly integrated into diverse use cases beyond speculative trading:

Cross-border Transfers: Offer faster and cheaper alternatives to traditional remittance channels.

Decentralized Finance (DeFi): Serve as collateral, lending instruments, and liquidity tools in DeFi platforms.

Payment Systems: Act as digital cash in online and offline transactions.

Economic Stability Tools: Provide an alternative to unstable local currencies in developing regions.

US Regulation:

The recent GENIUS Act (2025) mandates that

USD-pegged stablecoins be fully backed by liquid reserves (cash, T-bills)

requires monthly public disclosure of reserve composition.

Supporters say this boosts credibility and adoption.

Critics argue it should also tighten AML controls and limit big-tech issuers.

Global Coordination:

Authorities (IMF, BIS, FSB) recommend a risk-based regulatory framework.

This would cover issuers, reserve managers, exchanges and wallets alike.

Cross-border stablecoins (so-called “global stablecoins”) especially call for international oversight to mitigate spillovers.

Industry-Regulator Collaboration:

Experts suggest stablecoin firms work with regulators to design rules that address risks without stifling innovation.

Potential measures include reserve audits, capital requirements for issuers, and robust consumer protections.

Future Outlook:

With estimates projecting stablecoins could hit ~$2 trillion by 2028, their influence is growing.

Stablecoins remain a diverse group of instruments, so policy may need to be tailored (e.g. stricter rules for unbacked coins).

The aim is to harness stablecoins’ efficiency (instant crypto payments) while ensuring they don’t destabilize the financial system.

Legal Status & Taxation: India currently treats all cryptocurrencies—including stablecoins- as Virtual Digital Assets (VDAs) under the Income Tax Act, 1961. Transfers of VDAs are taxed at 30% capital gains, with a 1% TDS on transactions above ₹50,000 per year.

Anti‑Money Laundering Oversight: Since March 2023, VDA service providers must register with FIU‑IND, act as ‘reporting entities’ under the Prevention of Money Laundering Act, 2002, maintain transaction records (including cash transactions over ₹10 lakh), and comply with KYC/AML standards.

Stablecoin Status: India does not distinguish stablecoins from other VDAs. There’s no legal framework recognising stablecoins; all fall under the same VDA classification.

Rise of CBDC (Digital Rupee): RBI's Digital Rupee (e‑rupee) is India’s official Central Bank Digital Currency (CBDC), seen as the regulated alternative to stablecoins. Retail e‑rupee circulation surged to ₹1,016 crore by March 2025 (from ₹234 crore a year earlier).

The CBDC is designed for programmable, traceable payments (e.g., DBT schemes), and is gradually being integrated via UPI and payment apps.

Question 1: With reference to ‘Bitcoins’, sometimes seen in the news, which of the following statements is/are correct? (UPSC Prelims 2016)

Bitcoins are tracked by the Central Banks of the countries.

Anyone with a Bitcoin address can send and receive Bitcoins from anyone else with a Bitcoin address.

Online payments can be sent without either side knowing the identity of the other.

Select the correct answer using the code given below:

(a) 1 and 2 only

(b) 2 and 3 only

(c) 3 only

(d) 1, 2 and 3

Answer: (d)

Q. What is a stablecoin?

A.A stablecoin is a cryptocurrency pegged to an asset (usually a fiat currency) to keep its value steady. It holds reserve assets so its price stays fixed to its peg (e.g. 1 USD).

Q. How do stablecoins maintain price stability?

A.Most stablecoins keep reserves equal to their circulating supply (fiat cash, bonds or crypto) to maintain the peg. Algorithmic stablecoins adjust their supply via smart contracts if demand changes.

Q. What are the main types of stablecoins?

A.Fiat-backed: 1:1 reserves in fiat (e.g. USDT, USDC). Crypto-backed: over-collateralized by crypto (e.g. Dai). Asset-backed: backed by commodities (e.g. gold). Algorithmic: no reserves, rely on automated mint/burn (e.g. TerraUSD*).

Q.What risks do stablecoins pose?

A.They can lose their peg if reserves dry up or algorithms fail. Large stablecoins can trigger market contagion if they collapse. Lack of transparency in reserves and weak regulation are also major concerns.

Q.What did the U.S. GENIUS Act (2025) do for stablecoins?

A.It created a regulatory framework requiring USD-pegged stablecoins to be fully backed by liquid assets (cash or T-bills) and to publicly disclose reserve compositions each month. This law aims to boost confidence and prevent runs.

Stablecoins play a key role in linking traditional finance with the crypto world. They enable instant crypto transactions and serve as “digital cash” for traders, but they carry unique risks.Recent U.S. actions (GENIUS Act, FSOC review) reflect growing concern that, at scale, stablecoins could threaten financial stability. International bodies (IMF, FSB) urge coordinated, risk-based regulation to safeguard users and markets. For UPSC aspirants, understanding stablecoins is important both as a digital payment innovation and as a focus of global financial policy.

Internal Linking Suggestions

How to Begin Your UPSC Preparation : The Ultimate Guide For Beginners

UPSC Previous Year Question Papers with Answers PDF - Prelims & Mains (2014-2024)

40 Most Important Supreme Court Judgements of India : Landmark Judgements UPSC

Article 32 of the Indian Constitution: Right to Constitutional Remedies, 5 Writs, Significance

Parliamentary Committees in India: Functions, Types & Significance, UPSC Notes

How to Prepare Current Affairs for UPSC Exam: A Comprehensive Guide

51st G7 Summit 2025 – Countries, Key Issues, India’s Role & UPSC

External Linking Suggestions

UPSC Official Website – Syllabus & Notification: https://upsc.gov.in/

Press Information Bureau – Government Announcements: https://pib.gov.in/

NCERT Official Website – Standard Books for UPSC: https://ncert.nic.in