Union Budget 2026 Analysis: PDF Download & UPSC Highlights

The Union Budget 2026-27, presented on February 1, 2026, targets a fiscal deficit of 4.3% of GDP. It introduces the New Income Tax Act 2025, allocates ₹12.2 lakh crore for capital expenditure, and outlines three specific "Kartavyas" to achieve a Viksit Bharat. Major reforms include the Biopharma SHAKTI fund, STT hikes, and rationalized customs duties.

Gajendra Singh Godara

10

mins read

The Union Budget is the Annual Financial Statement of the Government of India, detailing estimated receipts and expenditures for the upcoming financial year. Article 112 of the Indian Constitution mandates this presentation. The government usually sets the Union Budget date for February 1. This helps get approval before the new financial year starts on April 1.

The Union Budget 2026-27 provides a comprehensive roadmap for various Sectors of Indian Economy, ranging from high-tech biopharma to traditional agriculture.

Union Budget 2026-27 PDF Download and Document Structure

For aspirants wishing to read the primary sources, the "Budget" is not a single document but a set of papers. You can access these on the official website (indiabudget.gov.in). The key documents to download include:

Annual Financial Statement (AFS): The constitutional document under Article 112.

Finance Bill: The legal instrument to implement tax changes (Article 110).

Key Features of Budget: A graphical summary useful for quick revision.

Macro-Economic Framework Statement: Mandated by the FRBM Act, evaluating growth prospects.

Finance Minister Nirmala Sitharaman presented the Union Budget 2026-27 on February 1, 2026, from "Kartavya Bhawan". This budget operates on the core philosophy of "Action over Ambivalence" and "Reform over Rhetoric".

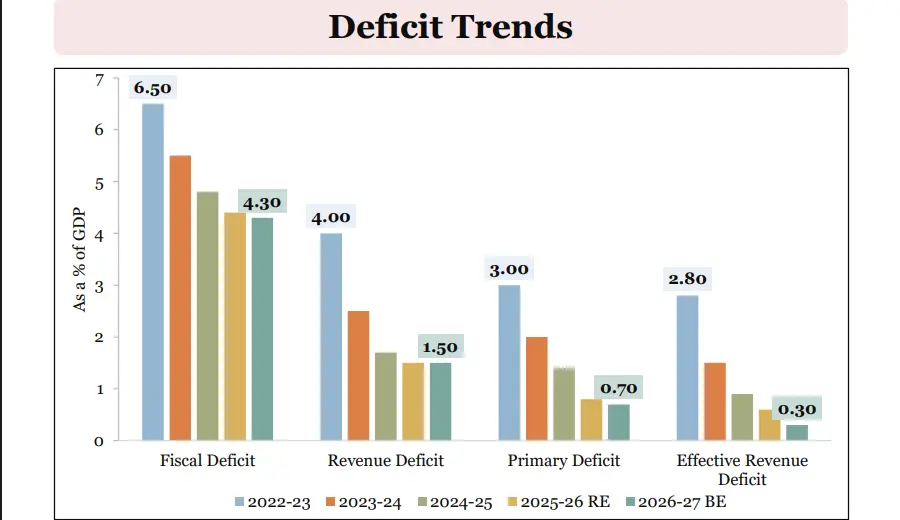

Fiscal Consolidation and Deficit Targets for 2026-27

The Union Budget 2026-27 highlights a distinct path toward fiscal consolidation. Finance Minister Nirmala Sitharaman affirmed that the government fulfilled its commitment to reduce the deficit below 4.5% by 2025-26.

Key Fiscal Statistics (BE 2026-27):

Fiscal Deficit: The target for BE 2026-27 is estimated at 4.3% of GDP.

Total Expenditure: The total spending is projected at ₹53.5 lakh crore.

Capital Expenditure (Capex): The allocation stands at ₹12.2 lakh crore, an increase from ₹11.2 lakh crore in the previous cycle.

Net Tax Receipts: Estimated at ₹28.7 lakh crore.

Gross Market Borrowings: Estimated at ₹17.2 lakh crore.

Debt-to-GDP Ratio: Projected at 55.6% for BE 2026-27, aimed at freeing resources for priority sectors.

This fiscal prudence aligns with the Economic Survey 2026 Summary, which projects a real growth rate of 6.8%–7.2%.

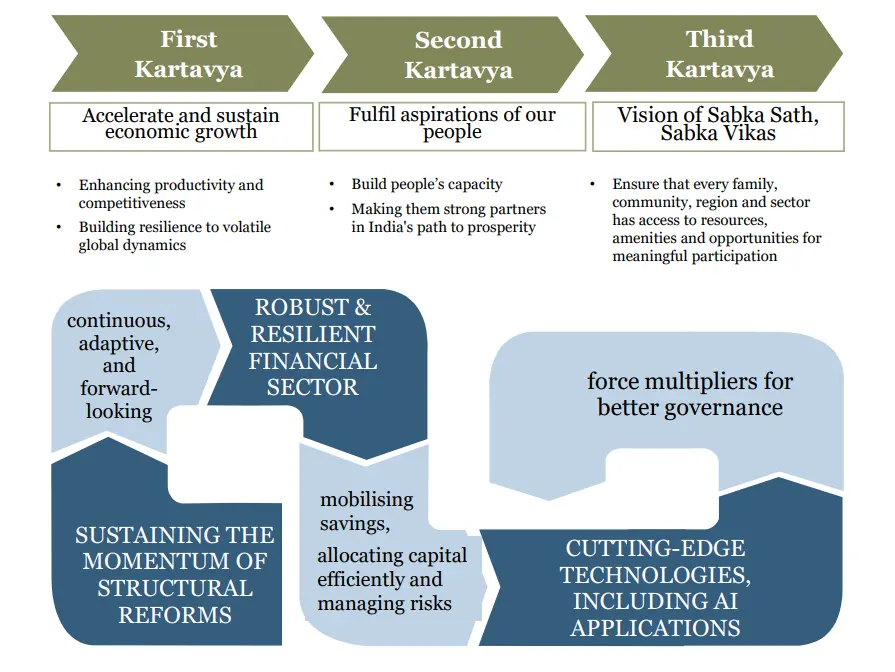

The 2026 Union Budget of India emphasizes a shift from entitlement to duty, structured around three central "Kartavyas" (Duties) aimed at accelerating growth and fulfilling aspirations.

Part A: The Three Kartavyas & Strategic Pillars

The Budget is structured around three "Kartavyas" (Duties) that guide the allocation of resources.

1. First Kartavya: Accelerating Economic Growth

The primary duty focuses on increasing productivity and building resilience against global volatility. The government identified six intervention areas, including manufacturing scaling, infrastructure push, and energy security.

Manufacturing and Industry Initiatives:

Biopharma SHAKTI: A new fund with an outlay of ₹10,000 crore will support the domestic production of biologics and biosimilars over five years. This aims to make India a global biopharma hub.

SME Growth Fund: A dedicated fund of ₹10,000 crore will incentivize high-performing micro-enterprises to become "Future Champions".

Legacy Clusters: The Ministry will rejuvenate 200 legacy industrial clusters through technology upgrades.

Chemical Parks: A challenge route cluster model will establish three dedicated Chemical Parks.

Infrastructure and Logistics:

High-Speed Rail: Seven new corridors will function as "growth connectors." Routes include Mumbai-Pune, Delhi-Varanasi, Hyderabad-Bengaluru, and Varanasi-Siliguri.

Freight Corridors: A new Dedicated Freight Corridor will connect Dankuni in the East to Surat in the West.

Waterways: The government plans to operationalize 20 new National Waterways, starting with NW-5 in Odisha to connect mineral-rich areas like Talcher to Paradip port.

City Economic Regions (CER): An allocation of ₹5,000 crore per CER over five years will support urban agglomerations based on specific growth drivers.

The expansion of High-Speed Rail and Dedicated Freight Corridors continues to be powered by the Pm Gati Shakti Scheme, ensuring integrated planning and synchronized implementation of multi-modal connectivity.

2. Second Kartavya: Fulfilling Aspirations

This duty targets capacity building. The budget notes that 25 crore individuals exited multidimensional poverty in the last decade.

Social Infrastructure (Health & Education):

STEM Education: The government will establish one girls' hostel in every district to support female students in STEM institutions.

Medical Tourism: Five Regional Medical Hubs will combine healthcare, education, and research to attract international patients.

Mental Health: Authorities will establish a new NIMHANS-2 in North India and upgrade institutes in Ranchi and Tezpur.

Creative Economy: The Indian Institute of Creative Technologies will set up AVGC (Animation, Visual Effects, Gaming, Comics) labs in 15,000 schools.

Sports: A Khelo India Mission will launch to transform the sports sector over the next decade.

3. Third Kartavya: Sabka Sath, Sabka Vikas

This duty aligns with equitable distribution. It prioritizes access to resources for the "Purvodaya" (Eastern) states, women, and the agricultural sector.

Agriculture and Allied Sectors:

Bharat-VISTAAR: This multilingual AI tool integrates AgriStack portals with ICAR agricultural practices to provide customized advice to farmers.

Aquaculture: Fish caught by Indian vessels in the Exclusive Economic Zone (EEZ) is now duty-free.

Cooperative Support: Deduction limits for cooperatives now extend to the supply of cattle feed and cotton seeds.

High-Value Crops: New programs support the cultivation of cashew, cocoa, and sandalwood.

Students referring to upsc economy notes should link these supply-side interventions to the broader concept of national income accounting.

Alongside Bharat-VISTAAR, the government emphasized the Pm Dhan Dhaanya Krishi Yojana to ensure food security and enhance the income of small and marginal farmers through better crop diversification.

Part B: Tax Reforms & Financial Bill

The Part B of the budget speech focuses on direct and indirect taxation. A major structural reform is the introduction of the New Income Tax Act, 2025, which replaces the 1961 Act. This new legislation takes effect from April 1, 2026.

Direct Tax Proposals

The income tax union budget announcements aim to simplify compliance and broaden the tax base.

Buyback Tax: Companies will no longer pay tax on share buybacks. Instead, the recipient shareholder pays capital gains tax. This closes a specific arbitrage loop.

TCS Reduction: The Tax Collected at Source (TCS) on overseas tour packages drops from the previous slabs of 5% and 20% to a flat 2%.

Safe Harbour for IT: The turnover threshold for availing "Safe Harbour" norms in the IT sector increases from ₹300 crore to ₹2,000 crore.

Foreign Asset Disclosure Scheme: A one-time, 6-month disclosure scheme allows taxpayers to declare foreign assets below a certain threshold to avoid prosecution. This applies to students and professionals.

Revising Returns: Revisers can file revised returns by paying a nominal fee, which extends the timeline from December 31 to March 31.

TDS on Manpower: The provisions explicitly include the supply of manpower services at a rate of 1% or 2%.

Exemption from Income Tax: Non-residents providing capital goods to toll manufacturers in bonded zones receive a 5-year income tax exemption.

Has the Minimum Alternate Tax (MAT) changed? Yes. The minimum alternate tax mat rate reduces to 14% and becomes a final tax, with no credit accumulation allowed after April 1, 2026.

Indirect Taxes and Customs Duty

The Union Budget 2026-27 PDF details extensive customs rationalization to support domestic manufacturing.

Critical Minerals: The government exempts Basic Customs Duty (BCD) for capital goods required to process critical minerals. This is vital for the energy transition.

Mobile and Electronics: The government extends BCD exemptions on lithium-ion cell manufacturing equipment.

CD exemptions on lithium-ion cell manufacturing equipment are extended.

Personal Imports: The tariff on dutiable goods imported for personal use reduces from 20% to 10%.

Healthcare: Authorities exempt customs duty on 17 specific cancer drugs and medicines for rare diseases.

Solar Glass: The government exempts BCD on the import of sodium antimonate to boost solar glass manufacturing.

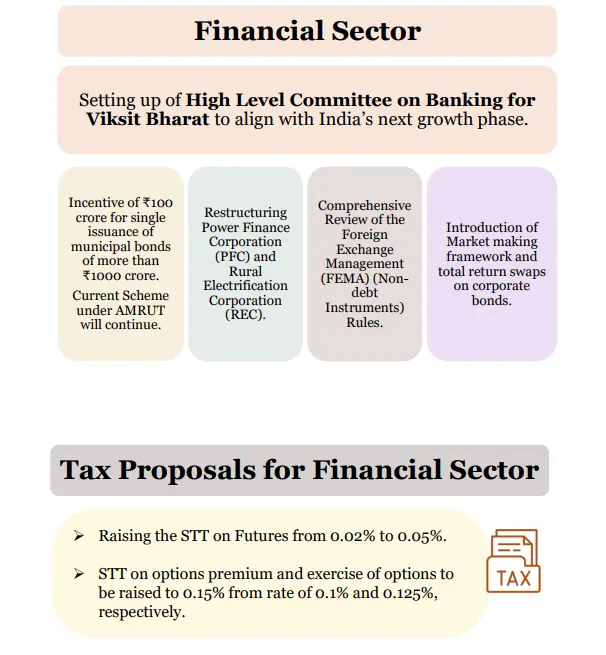

Financial Sector Reforms

To deepen the bond market and fund infrastructure, the budget proposes specific financial mechanisms.

Securities Transaction Tax (STT): The STT on Futures rises to 0.05% (from 0.02%) and on Options to 0.15%. This measure aims to curb excessive speculation in the derivatives market.

Municipal Bonds: The government offers a ₹100 crore incentive for municipal bond issuances exceeding ₹1,000 crore to improve urban financing.

Cloud Services Tax Holiday: Foreign cloud service providers using Indian data centre services receive a tax holiday until 2047.

Understanding these financial reforms helps clarify the components of gross domestic product (gdp)calculation and capital formation.

Join our WhatsApp Community

Article | Provision Name | Key Function & UPSC Relevance |

Article 110 | Definition of "Money Bill" | Defines bills dealing exclusively with taxation, borrowing, or the Consolidated Fund. The Finance Bill usually qualifies as a Money Bill, restricting Rajya Sabha's powers to rejection. |

Article 112 | Annual Financial Statement | Mandates the President to lay the statement of estimated receipts and expenditures before both Houses. This is the constitutional term for "Budget". |

Article 113 | Procedure w.r.t. Estimates | Distinguishes between "charged" expenditure (non-votable) and "voted" expenditure. Mandates that Lok Sabha must vote on Demands for Grants. |

Article 114 | Appropriation Bills | Provides legal authority to withdraw money from the Consolidated Fund. No money enters the economy without this Act. |

Article 115 | Supplementary Grants | Allows the government to request additional funds if the authorized amount for a service remains insufficient during the current fiscal year. |

Article 116 | Vote on Account | Authorizes the Lok Sabha to grant funds in advance (usually for 2 months) to keep the government running pending the full Budget's passage. |

Article 117 | Financial Bills | Covers bills involving expenditure from the Consolidated Fund that do not strictly qualify as Money Bills (Type I and Type II). |

Article 265 | Taxes by Authority of Law | Establishes that no tax shall be levied or collected except by authority of law. An executive order cannot impose a new tax. |

Article 266 | Consolidated Fund & Public Accounts | All revenues (Tax/Non-Tax) and loans flow into the Consolidated Fund. Public Accounts hold other public monies like PF deposits. |

Article 267 | Contingency Fund | A fund placed at the President's disposal to meet unforeseen expenditures (e.g., disasters) pending Parliamentary authorization. |

Note: The term "Budget" does not appear in the Constitution.

1. Ease of Doing Business

The budget prioritizes ease of doing business through the simplification of the tax code. The reduction of the TDS rate for manpower services and the automation of the "Safe Harbour" process for IT firms reduce the compliance burden. The establishment of the "Customs Integrated System" (CIS) to automate cargo clearance is another step toward frictionless trade.

2. Urbanization and Regional Development

The concept of City Economic Regions (CER) acknowledges that economic activity does not stop at municipal boundaries. By allocating ₹5,000 crore per CER, the budget encourages a cluster-based approach to urbanization. This is relevant for GS Paper 1 (Urbanization) and GS Paper 3 (Infrastructure).

3. Strategic Autonomy

The emphasis on critical minerals and the removal of customs duty on machinery for processing them highlights India's intent to secure its supply chains. This aligns with the "Swadeshi" push mentioned in the Economic Survey.

UPSC Prelims Pointers

Article 112: The constitutional basis for the "Annual Financial Statement".

Vote on Account: Article 116 allows the government to spend money for a part of the year before the full budget passes.

Finance Bill vs. Appropriation Bill: The Finance Bill (Article 110) handles taxes/revenue, while the Appropriation Bill (Article 114) authorizes expenditure.

Effective Revenue Deficit: Aspirants must track the difference between the Revenue Deficit and grants for creation of capital assets.

Mains Answer Writing Fodder

GS Paper 3 (Economy): Use the "Biopharma SHAKTI" and "Bharat-VISTAAR" schemes as examples of technology integration in industry and agriculture.

GS Paper 2 (Health): Cite the "Regional Medical Hubs" and "NIMHANS-2" when discussing health infrastructure gaps.

GS Paper 3 (Infrastructure): The shift to "Warehouse operator-centric systems" illustrates ease of doing business reforms.

Add as a preferred Source on Google

Frequently asked question (FAQs)

What is the Union Budget date for 2026?

What is the fiscal deficit target for 2026-27?

Are there changes to capital gains on share buybacks?

What is the Biopharma SHAKTI scheme?

What is the new Foreign Asset Disclosure Scheme?

The Union Budget for 2026-27 establishes a clear plan for "Viksit Bharat." It balances a high Capital Expenditure of ₹12.2 lakh crore with careful spending. The vision is to keep the deficit at 4.3%.

The government plans to replace the old Income Tax Act of 1961 with the New Income Tax Act 2025. This change aims to make it easier for citizens to comply with tax rules.

The budget includes funds like the ₹10,000 crore Biopharma SHAKTI fund. It also introduces Bharat-VISTAAR for agriculture. These efforts focus on modernizing important parts of the economy. At the same time, the budget keeps support for vulnerable groups through programs like SHE Marts.

Gajendra Singh Godara is an IIT Bombay graduate and a UPSC aspirant with 4 attempts, including multiple Prelims and Mains appearances. He specializes in Polity, Modern History, International Relations, and Economy. At PadhAI, Gajendra leverages his firsthand exam experience to simplify complex concepts, creating high-efficiency study materials that help aspirants save time and stay focused.

No comments yet. Be the first to join the discussion!