Subhadra Yojana 2026: Eligibility, Process, Benefits & Status Check

Gajendra Singh Godara

11

mins read

Subhadra Yojana is Odisha's flagship cash support scheme for women.

Eligible women get ₹10,000 a year, paid in two installments of ₹5,000, straight into their Aadhaar-linked bank accounts. Over five years that adds up to ₹50,000.

The scheme launched in September 2024, is named after Goddess Subhadra, the sister of Lord Jagannath, and by 2026 it reaches over one crore women across the state.

If you are preparing for UPSC or a state PCS, this scheme is a ready-made governance case study.

It sits at the meeting point of women's empowerment, Direct Benefit Transfer, digital financial inclusion, and the wider debate on cash transfers to women.

If you or someone in your family is a beneficiary, you also need the practical parts: how to apply, how to check status, how to find your name in the list, and what the mandatory e-KYC verification means for your payment. This guide covers both, in plain language.

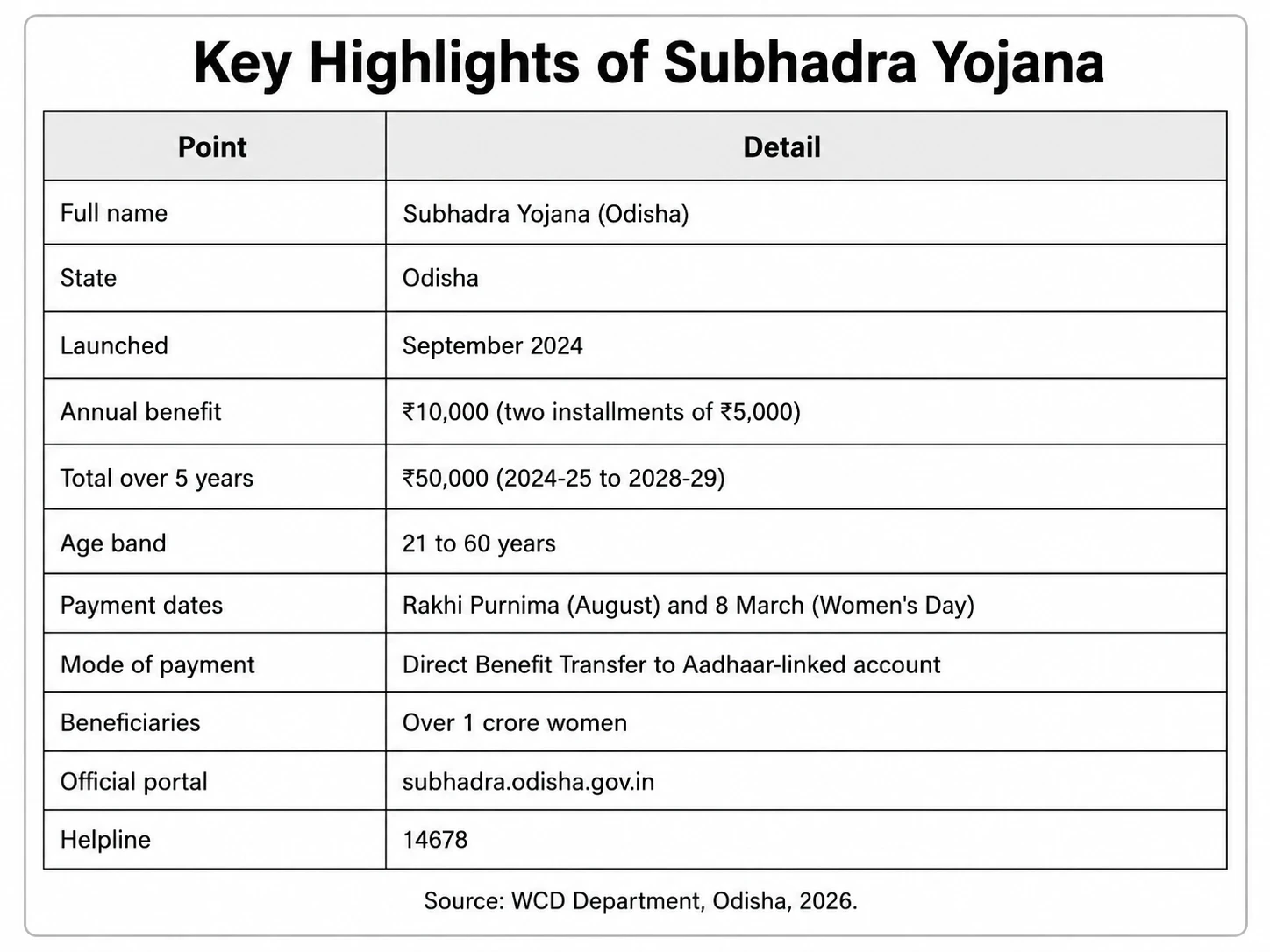

Point | Detail |

Full name | Subhadra Yojana (Odisha) |

State | Odisha |

Launched | September 2024 |

Annual benefit | ₹10,000 (two installments of ₹5,000) |

Total over 5 years | ₹50,000 (2024-25 to 2028-29) |

Age band | 21 to 60 years |

Payment dates | Rakhi Purnima (August) and 8 March (Women's Day) |

Mode of payment | Direct Benefit Transfer to Aadhaar-linked account |

Beneficiaries | Over 1 crore women |

Official portal | |

Helpline | 14678 |

Join our WhatsApp Community

Subhadra Yojana is a women welfare scheme run by the Government of Odisha through its Women and Child Development (WCD) Department.

The core idea is simple. Every eligible woman between 21 and 60 years gets ₹10,000 each year, split into two equal payments of ₹5,000.

The money goes directly to her own bank account, and she is free to spend it however she wants, whether on household needs, a child's fees, healthcare, or savings.

A few features make Subhadra Yojana stand apart from a plain cash handout:

Two festival-linked payments. The two installments are timed to reach women on Rakhi Purnima in August and on International Women's Day on 8 March. That fixed rhythm is deliberate, since it makes the benefit predictable.

Subhadra Debit Card. Every approved beneficiary gets a dedicated ATM-cum-debit card for cash withdrawal and digital payments.

Digital transaction reward. The top 100 women by digital transactions in each gram panchayat or urban local body earn an extra ₹500 a year. This is a nudge to build real digital banking habits.

Five-year window. The scheme runs from 2024-25 to 2028-29, so a woman who stays eligible can receive up to ₹50,000 in total.

In the name, the scheme is deliberately rooted in Odia culture. Subhadra is the sister of Lord Jagannath and Balabhadra, and the trio is worshipped at the Puri temple.

Naming a women's scheme after her gives it an emotional pull that a plain acronym never could.

Subhadra Yojana Summary Table

Parameter | Details |

Type | State women welfare and cash transfer scheme |

Implementing body | Women and Child Development Department, Odisha |

Annual assistance | ₹10,000 (2 x ₹5,000) |

Total assistance | ₹50,000 over five years |

Age eligibility | 21 to 60 years |

Family income ceiling | Below ₹2.5 lakh per year (or NFSA / SFSS ration card) |

Payment route | DBT to Aadhaar-seeded, NPCI-mapped bank account |

Verification | Aadhaar-based e-KYC, now Face Authentication e-KYC |

Extra features | Subhadra Debit Card, ₹500 digital reward |

Beneficiaries | Over 1 crore women |

The scheme is not only about handing out money. The Odisha government lists a set of connected goals that make it useful for a Mains answer:

Financial empowerment. Give women direct cash so they can manage household and personal expenses on their own terms.

Economic inclusion. Make sure women from weaker sections receive government benefits without any middleman skimming the amount.

Digital literacy. Push women toward digital banking through the debit card and the ₹500 incentive.

Cultural connect. Tie the scheme to Odisha's traditions by naming it after Goddess Subhadra.

Wide coverage. Reach more than one crore women across the state over the five-year period.

Add as a preferred Source on Google

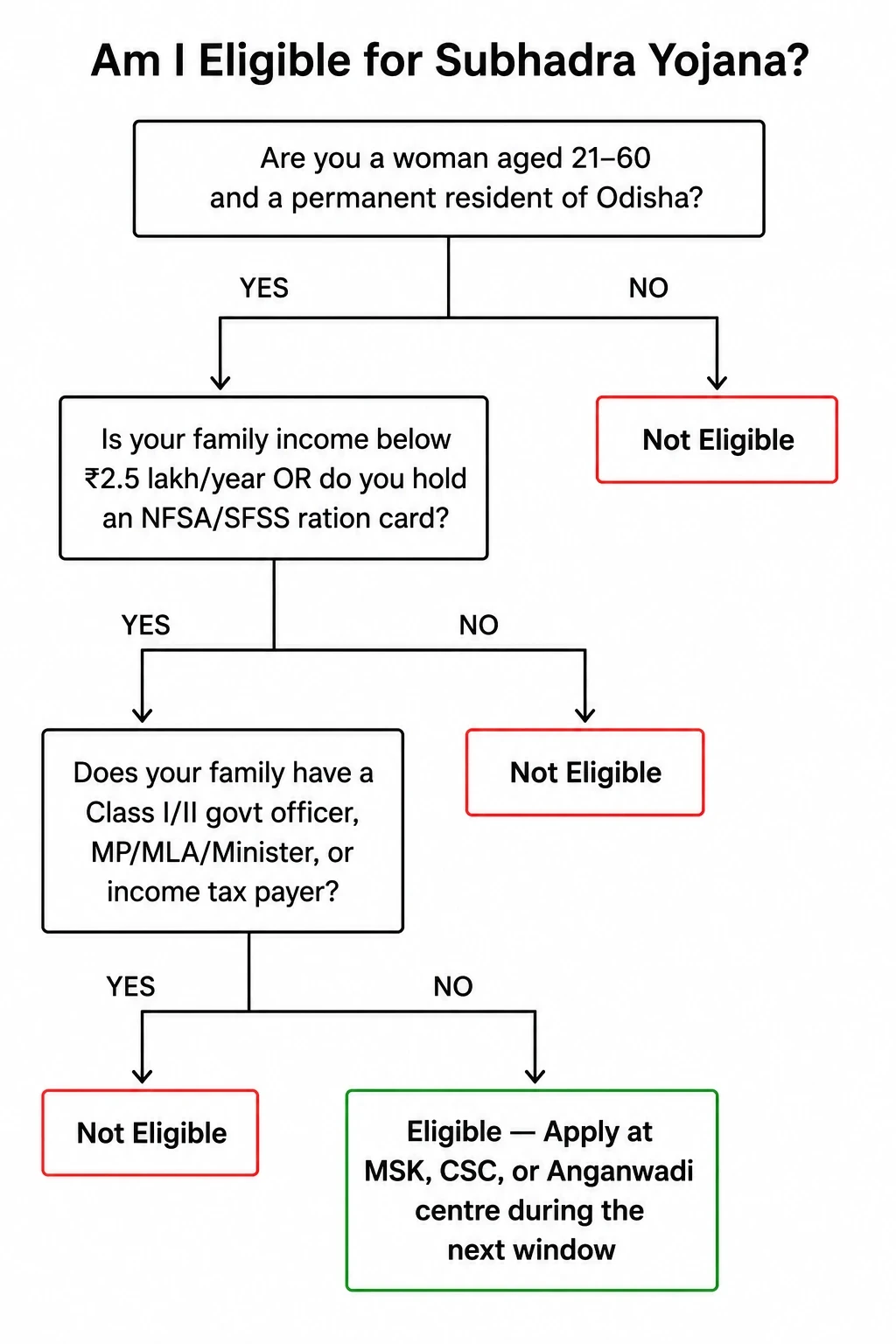

To qualify for the Subhadra Yojana odisha, a woman must meet every condition below, not just some of them.

Condition | Requirement |

Gender | Only women are eligible |

Age | Between 21 and 60 years at the time of applying |

Residence | Permanent resident of Odisha with valid domicile proof |

Income | Family income below ₹2.5 lakh a year, or an NFSA / SFSS ration card |

Bank account | Single-holder, Aadhaar-linked, DBT-enabled account |

Verification | Aadhaar-based e-KYC is compulsory |

A useful nuance for aspirants. A woman who holds an NFSA (National Food Security Act) or State Food Security Scheme (SFSS) ration card is treated as automatically within the income limit, so she does not need a separate income certificate.

Women without these cards can still apply if they produce a valid income certificate showing family income below ₹2.5 lakh.

Both married and unmarried women can apply, as long as they meet the age and income conditions.

Who is not eligible for Subhadra Yojana

Some households are excluded by design so the money reaches those who need it more. After verification, the following are left out:

Women whose family has a current or former MP, MLA, or Minister

Women with a family member serving as a Class I or Class II government officer

Women from income-tax paying families

Women already getting ₹1,500 or more a month (₹18,000 a year or more) from another government scheme

Subhadra Yojana gives more than just cash. The full set of benefits looks like this:

Annual support of ₹10,000, in two installments of ₹5,000, to help with regular household costs.

₹50,000 over five years, giving sustained support rather than a one-time payout.

Direct bank transfer with no middlemen, since the money moves through DBT into an Aadhaar-linked account.

Subhadra Debit Card for easy withdrawal and digital spending.

₹500 digital reward for the top 100 women by digital transactions in each gram panchayat or urban local body.

No repayment. The money is a grant, not a loan. A beneficiary never has to pay it back.

Here expectations need a small reality check. The Subhadra Yojana online application route exists on the portal, but for most women the process runs through service centres with Aadhaar-based e-KYC done in person.

The government also runs fixed registration windows rather than keeping applications open all year.

The 2026-27 registration window ran from 1 to 30 April 2026 and is now closed, so fresh applications are expected to open again in a later cycle.

Watch subhadra.odisha.gov.in for the next window.

Documents you need

Aadhaar card (with a linked mobile number for OTP)

Bank passbook of a single-holder, Aadhaar-linked account

NFSA or SFSS ration card, or an income certificate

Address or domicile proof

Passport-size photograph

Where to apply

Applications are collected free of cost at Mo Seva Kendra (MSK), Common Service Centres (CSC or Jana Seva Kendra), Anganwadi centres, and Block Development Office or ULB offices.

The government has clearly said the form, scanning, and e-KYC are all free, so never pay a fee to anyone for it.

Step-by-step application

Collect the free Subhadra Yojana form from an MSK, CSC, or Anganwadi centre, or open subhadra.odisha.gov.in when the window is live.

Enter your Aadhaar number and complete Aadhaar-based e-KYC through OTP or biometric or Face Authentication.

Your name, date of birth, and address are pulled from UIDAI records, so check them carefully. If your form differs from Aadhaar, the Aadhaar data is treated as final.

Add bank details, that is account number, IFSC code, and confirm the account is Aadhaar-seeded.

Upload document scans and submit.

Save the Application Reference Number from the receipt. You need this 16-digit number for every future Subhadra Yojana status check.

A word of caution. Several unofficial websites offer a "Subhadra Yojana form PDF" or promise online registration outside the official window.

Use only subhadra.odisha.gov.in or a government service centre, and never enter your Aadhaar number on a site that is not the official portal.

A Subhadra Yojana status check tells you whether your application is pending, approved, or rejected, and whether your e-KYC and bank seeding are in order.

There are two layers to it, and understanding both saves a lot of confusion.

On the portal:

Open subhadra.odisha.gov.in and go to Beneficiary Login or Track Status.

Log in with your registered mobile number and OTP, or enter your Aadhaar or Application Reference Number.

The screen shows your application stage, e-KYC status, and installment status.

Look for two green signals: "eKYC Complete" and "NPCI Active". Both must be green before any money can land.

In your bank:

The portal shows your application stage, but the actual payment record sits with your Aadhaar-linked bank account, because the money arrives by DBT.

To confirm a credit, check your bank passbook, SMS alerts, or net banking.

If the portal says "paid" but nothing arrived, the problem is almost always your Aadhaar-bank seeding, not a rejection.

Here is the single most common trap. Aadhaar being "linked" to your account is not the same as being "NPCI-seeded for DBT".

Ask your bank specifically for "Aadhaar seeding or NPCI mapping for Subhadra DBT".

This is a separate bank-side step, and skipping it is the top reason payments bounce back even for approved women.

The Subhadra Yojana list name check 2026 lets you confirm whether your name made the approved beneficiary list before an installment cycle. Steps:

Open subhadra.odisha.gov.in and go to the beneficiary list or "Aadhaar Search" (Aadhaar Sandhan) section.

Enter your Aadhaar number or Application Reference Number.

If your record appears, your form is digitised and your name is in the system.

Common status meanings you will see: "Pending" means your application is still under field verification, "Approved" means you are cleared for the next transfer, and "Rejected" carries a reason.

The usual rejection reasons are pending e-KYC, an Aadhaar not seeded with the bank, wrong personal details, incomplete document uploads, or a duplicate application.

Most of these can be fixed at your nearest MSK or CSC and resubmitted.

Subhadra Yojana Verification Deadline and e-KYC Update

This is the most important Subhadra Yojana verification deadline point for 2026, and many women missed it.

Face Authentication e-KYC is now mandatory to receive 2026 installments. This applies to everyone, including women who received all earlier installments smoothly.

If your e-KYC is pending, your payment can be held even when you are otherwise eligible.

How the verification works in practice:

The Subhadra Yojana verification deadline is set a few weeks before each scheduled installment date. Only beneficiaries verified before the cutoff for a cycle get paid in that cycle.

Complete Face Authentication e-KYC on the Subhadra portal or the SUBHADRA app, then recheck your status after 3 to 5 days to confirm it shows "eKYC Complete".

If your fingerprint or face does not match, you may be asked to update biometrics at a nearby post office or service centre.

If your money stopped in 2026 even though your bank account is fine, pending Face e-KYC is the most likely reason.

Earlier in 2026, Deputy Chief Minister Pravati Parida confirmed a review for women who missed the 4th installment, including new applicants and those with pending e-KYC, so completing verification is the surest way to get back into the payment cycle.

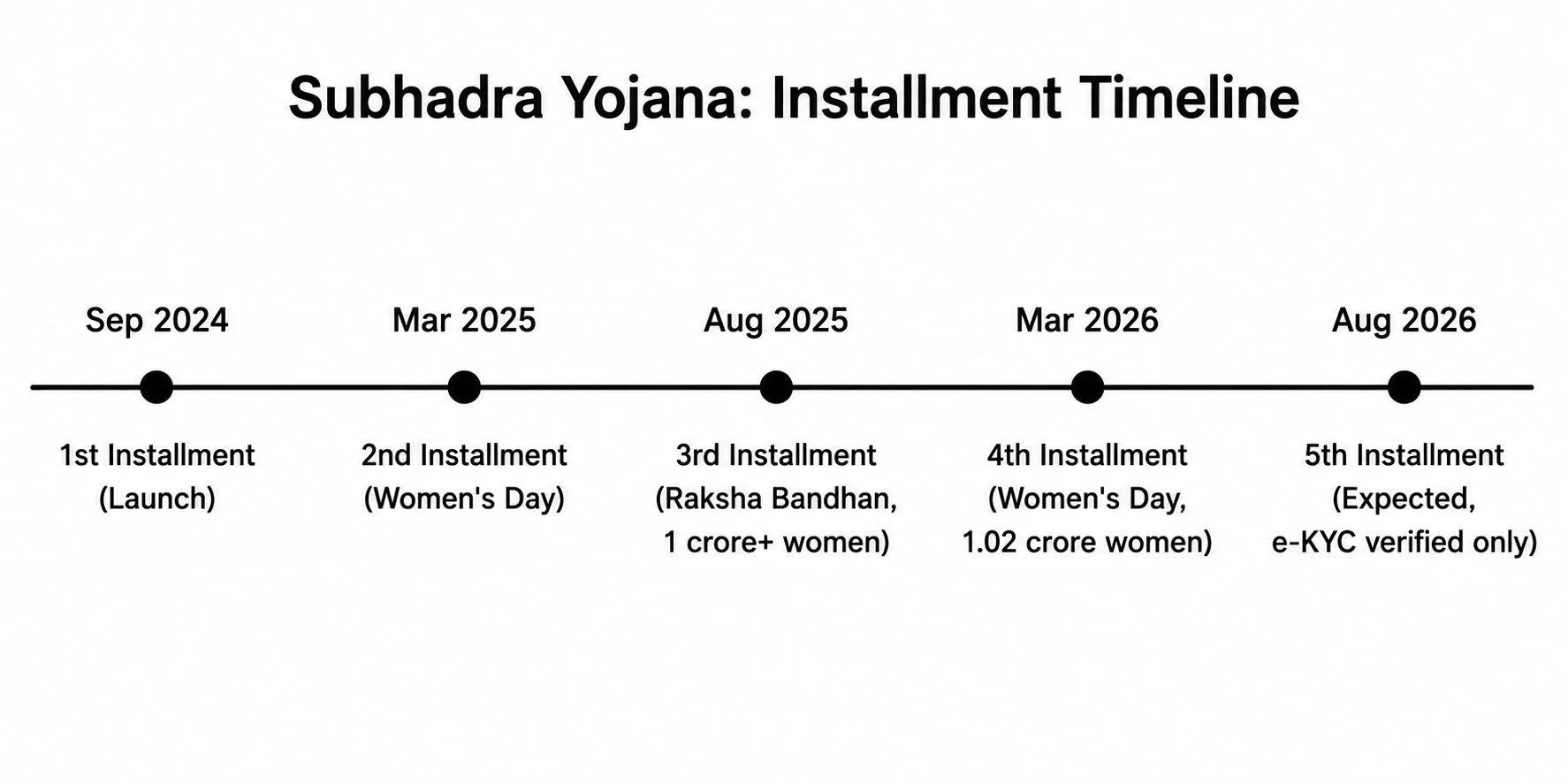

Subhadra Yojana Installment Dates

Beneficiaries track Subhadra Yojana installment dates closely. Unlike monthly schemes, Subhadra pays twice a year on two fixed occasions, so the pattern is easy to remember.

The recent cycle looked like this:

Installment | When | Status |

3rd installment | Raksha Bandhan, August 2025 | Paid to over 1 crore women |

4th installment | 8 March 2026 (Women's Day) | Paid to about 1.02 crore women |

5th installment | Around Raksha Bandhan, August 2026 | Expected, verified beneficiaries only |

By early 2026 the scheme had transferred over ₹2,100 crore in total. The 5th installment stays at ₹5,000.

The WCD department does not pre-announce an exact calendar date, so the safest way to confirm your payment is your own bank passbook rather than any third-party site promising precise dates.

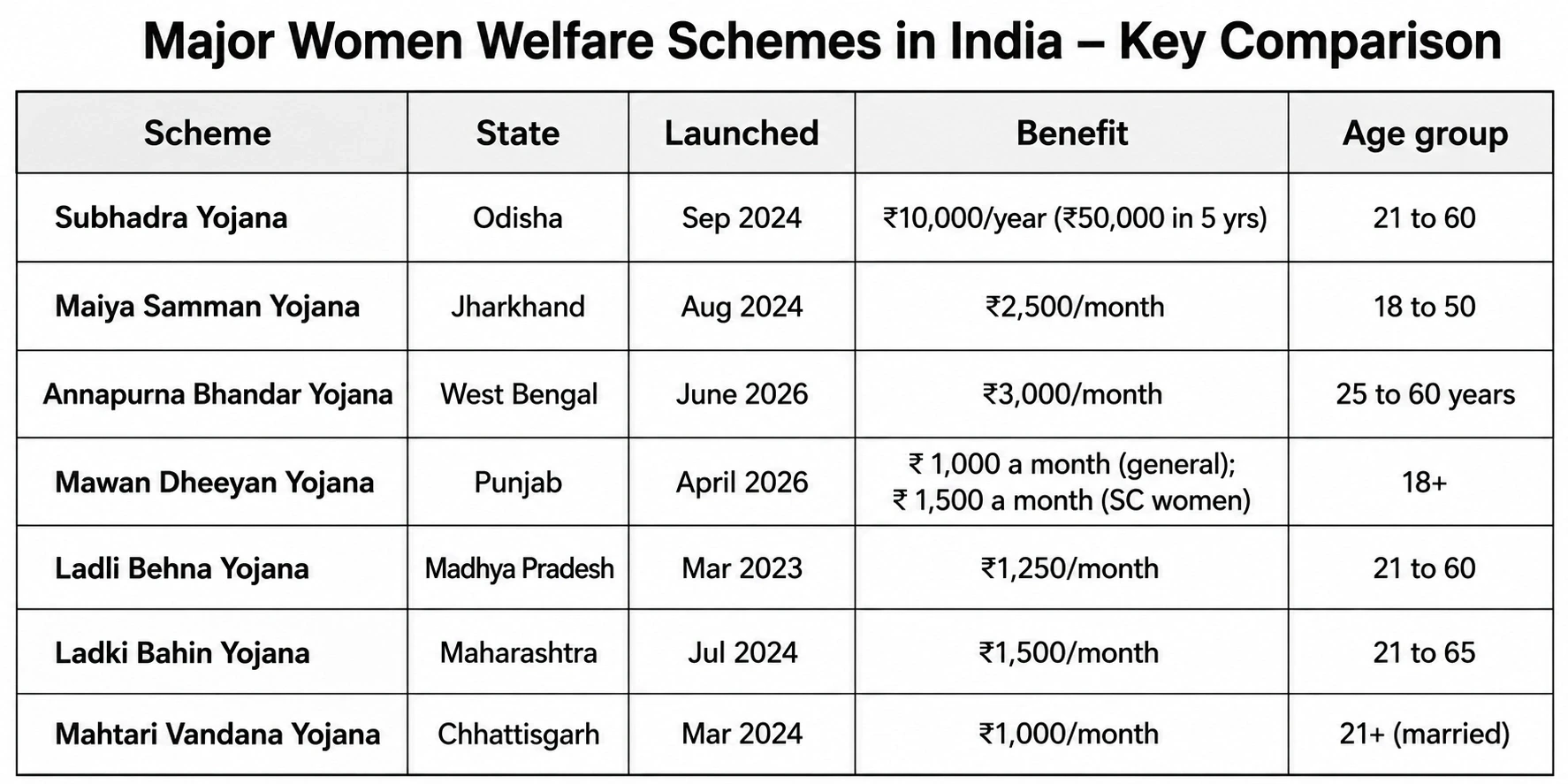

How Subhadra Yojana Compares With Other State Schemes

Odisha was not the first state to try direct cash for women, and a quick comparison is gold for a Mains answer, since it shows a clear all-India pattern.

Scheme | State | Launched | Benefit | Age group |

Subhadra Yojana | Odisha | Sep 2024 | ₹10,000/year (₹50,000 in 5 yrs) | 21 to 60 |

Jharkhand | Aug 2024 | ₹2,500/month | 18 to 50 | |

West Bengal | June 2026 | ₹3,000/month | 25 to 60 years | |

Punjab | April 2026 | ₹ 1,000 a month (general); ₹ 1,500 a month (SC women) | 18+ | |

Ladli Behna Yojana | Madhya Pradesh | Mar 2023 | ₹1,250/month | 21 to 60 |

Ladki Bahin Yojana | Maharashtra | Jul 2024 | ₹1,500/month | 21 to 65 |

Mahtari Vandana Yojana | Chhattisgarh | Mar 2024 | ₹1,000/month | 21+ (married) |

One design difference is worth noting. Most of these schemes pay monthly, while Subhadra Yojana pays a lump sum twice a year.

A monthly transfer helps with routine expenses, while a festival-linked lump sum suits bigger one-time needs.

That trade-off between frequency and size is a neat point to raise in an answer on how cash transfer schemes are designed.

Why Subhadra Yojana Matters for UPSC

A scheme like this is not just trivia. It links to three different GS papers, and the same facts can be reused across all of them.

Prelims pointers

Lock these clean facts in for Prelims:

Scheme: Subhadra Yojana, run by Odisha (WCD Department)

Launched: September 2024

Benefit: ₹10,000 a year in two ₹5,000 installments, ₹50,000 over five years

Payment dates: Rakhi Purnima (August) and 8 March

Age band: 21 to 60 years

Income cap: family income below ₹2.5 lakh (or NFSA / SFSS card)

Mode: DBT to Aadhaar-linked account, with Face e-KYC and a Subhadra Debit Card

Helpline: 14678, portal subhadra.odisha.gov.in

The Mains angle and the cash transfer debate

This is where Subhadra Yojana earns its place in GS papers.

GS2 (Governance and welfare): It is a clean case study of DBT, beneficiary targeting, e-KYC-based verification, and the role of a state government in welfare delivery.

It fits the constitutional spirit of the Directive Principles, especially Article 39(a) on adequate means of livelihood, Article 41 on public assistance in cases of want, and Article 46 on the economic interests of weaker sections.

Article 15(3), which lets the state make special provisions for women, gives such schemes their constitutional base.

GS1 (Society): A cash transfer aimed at women raises her bargaining power inside the household and gives her a say in family spending.

The digital literacy angle, through the debit card and the ₹500 reward, adds a financial-inclusion dimension that connects to digital India initiatives like PM Jan Dhan Yojana.

GS3 (Economy): Here lies the real debate. Supporters argue that cash to women improves nutrition, health, and human capital, and builds digital and banking habits.

Critics flag the fiscal load on state budgets, the risk of duplication with central schemes, and the wider welfare-versus-freebies question.

The RBI and successive Finance Commissions have repeatedly cautioned states against off-budget liabilities and unfunded subsidies. Article 282, which allows discretionary grants for a public purpose, is often cited in this argument.

The trick in a Mains answer is to avoid picking a side too fast.

Show that you understand the empowerment and inclusion case for Subhadra Yojana, weigh it against the fiscal and targeting concerns, and close with a balanced view on how such transfers can be made sustainable and better targeted.

Frequently asked question (FAQs)

How much money is given under Subhadra Yojana?

How can I do a Subhadra Yojana status check?

Can I do Subhadra Yojana online apply any time?

Why did my Subhadra Yojana installment stop in 2026?

Is Subhadra Yojana useful for the UPSC exam?

Subhadra Yojana is more than a twice-a-year ₹5,000 transfer. For over one crore women in Odisha it is a steady, festival-linked source of independence and a first step into formal digital banking, and for an aspirant it is a ready-made case study that ties welfare, gender, and state finances together.

Keep the core facts handy for Prelims, hold both sides of the cash transfer debate for Mains, and if you are a beneficiary, finish your Face e-KYC and watch your bank passbook rather than any third-party site.

Research methodology

PadhAI's research methodology ensures every article is accurate, UPSC-ready, and beginner-friendly. We curate current affairs analysis based on UPSC exam relevance by cross-referencing The Hindu, Indian Express, and PIB. General Studies (GS) topics are drafted from NCERTs and standard books such as M. Laxmikanth, Spectrum, and GC Leong, then reviewed by subject matter experts to eliminate factual errors. Additionally, we update aspirants with verified government exam notifications alongside expert blogs suggesting the best resources, syllabus, and comprehensive Prelims and Mains strategies.

Gajendra Singh Godara is an IIT Bombay graduate and a UPSC aspirant with 4 attempts, including multiple Prelims and Mains appearances. He specializes in Polity, Modern History, International Relations, and Economy. At PadhAI, Gajendra leverages his firsthand exam experience to simplify complex concepts, creating high-efficiency study materials that help aspirants save time and stay focused.

No comments yet. Be the first to join the discussion!